Balance sheet tracks the change in the company’s cash balance from one year to the next. However, it does not tell us why the cash balance changes. Income statement is prepared under the accrual basis of accounting, the revenues reported may not have been collected or turned into cash.

Statement of Cash Flows reports the cash generated and used during specified time interval. It acts as a bridge between the Income Statement and Balance Sheet by showing how money moved in and out of the business. Cash Flow is defined as Inflows and outflows of cash and cash equivalents. Cash Equivalents include cash held as bank deposits, short-term investments, and any easily cash-convertible assets.

Component of Statement of Cash Flows

The statement of cash flows has given better idea as to where cash is generated from and where cash is used. Statement of Cash Flows consists of cash flows from following

- Operating activities

- Investing Activities

- Financing Activities

Operating Activities

Cash flows from operating activities are those related to the company’s operations-related current assets and current liabilities. Items classified under operating activities are an primarily revenue-producing activity. Examples of cash inflows operating activities are:

- Sale of goods and services

- Settlement of insurance claims

- Supplier refunds

- Income from Interest

Examples of cash outflows operating activities are:

- Employees Salary

- Payments to suppliers

- Income Tax

- Settlement of asset retirement obligations

- Interest Payment

Adjustments for various items are done in net income. Depreciation and amortization expenses are deducted from revenues when calculating profits, this expense is not paid or owed to anyone. So the depreciation and amortization expense will have to be added back in full to the net income. Any deferred taxes will also have to be added to net income.

The next adjustment is for non-cash base salaries. Part of salary may include stock-based compensation. While this compensation is recognized as an expense on the income statement, this, again is cash not paid to employees.

Investing activities

Cash flows from investing activities are those related to the company’s non-current assets. For example payments made to acquire long-term assets, purchase or sale of securities issued by other entities. Examples of investing activities include the following

- Long-term Investments

- Purchase of assets like land, building and equipment

- Sale of assets

- Purchase of investment instruments

These investments are not reported on the income statement. Any increase in investment assets will mean that the company has spent cash to buy these assets and will result in a reduction in cash.

Financing activities

Cash flows from financing activities are those related to the company’s non-current liabilities and shareholders’ equity. Items that may be included in the financing activities are:

- Sale or repurchase of company stock

- Issuance of debt, such as bonds

- Repayment of debt

- Dividends payment

- Deferred Income Taxes

- Retained Earnings

Any increase in financing activities would result in an increase in cash, and any decrease in financing activities would result in a decrease in cash. An increase in financing activities means that the company has raised additional capital from various sources, and so it has more cash on hand.

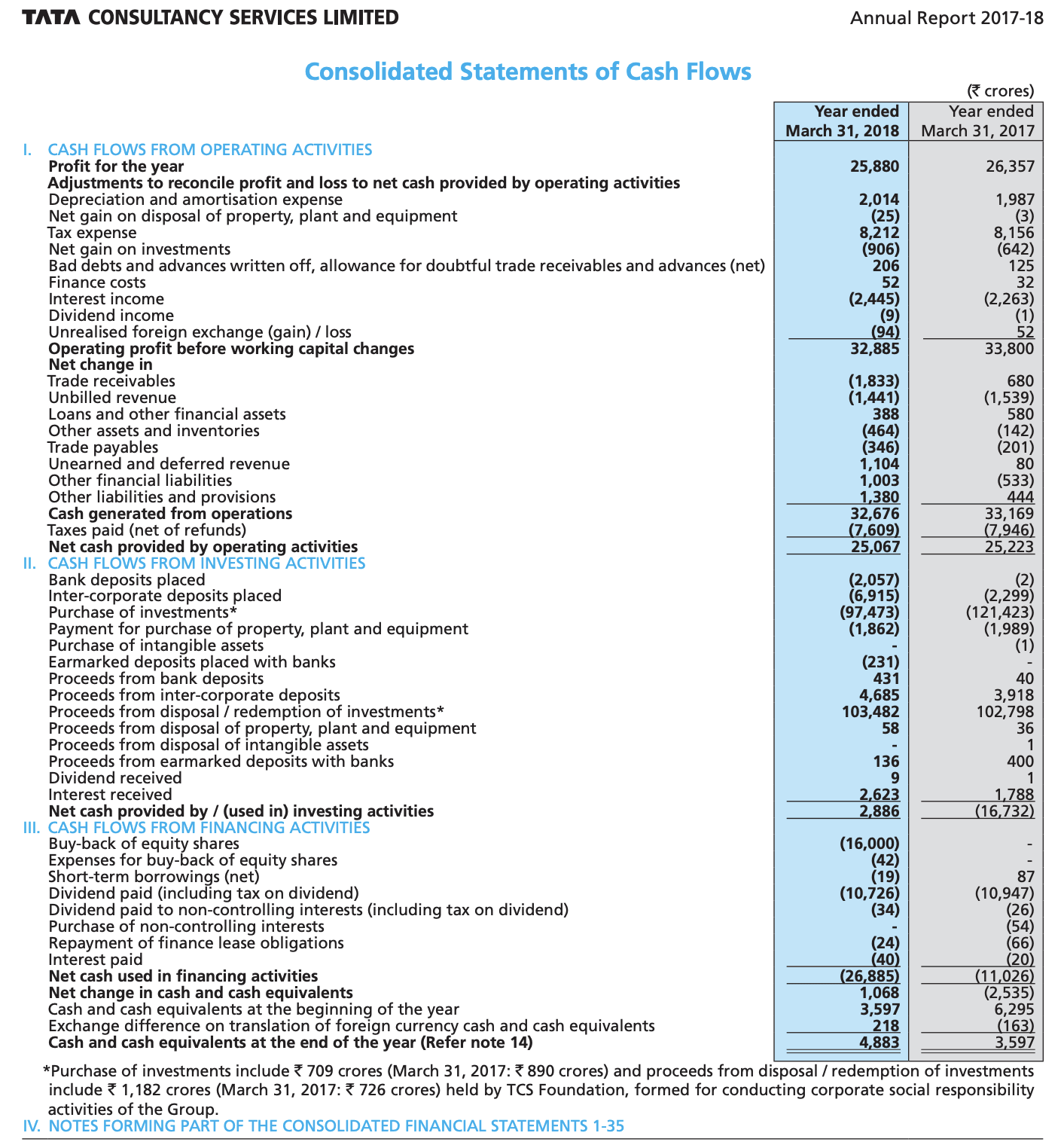

Statement of Cash Flows Example

Below is an example of TCS Statement of Cash Flows.

Above statement of cash flows has three columns.

- Financial items are listed in Column 1

- Column 2 contains numbers for just concluded year

- Column 3 contains numbers for year prior to just concluded year